Introduction

This paper describes the implementation of an automated quantitative FX trading strategy based on macro news data provided by RavenPack. RavenPack sources news from a variety of sources from which it produces an array of analytics (including sentiment, relevance and novelty) in real-time, and which are available historically.

We undertook the research and implemented the strategy in the Deltix QuantOffice research platform, a purpose-built C# development studio with embedded math, statistics and data libraries.

Our thesis was: does the arrival of macroeconomic news from the world’s largest economies bring additional volatility to the market? The historical data set used is described below:

- News Data from 1 March 2012 till 1 August 2012:

– More than 1.1 million messages

– Used subset of macro-economic news for US (287,000 records), Germany (7,800), EU (3,700) and Japan (14,400).

- Market Data from 1 March 2012 till 1 August 2012:

– Three currency pairs: EURUSD, USDJPY, EURJPY (bid/ask quotes)

– Approx 100 million market data messages.

- News data was filtered by the following news types:

– consumer-price-index

– producer-price-index

– unemployment

– retail-sales

– gross-domestic-product

– durable-goods

– interest-rate

– consumer-confidence

– home-sales-existing, home-sales-new

– current-account, current-account-surplus, current-account-deficit

– consumer-spending

– jobless-claims

– inflation

– trade-balance, trade-balance-deficit, trade-balance-surplus

- Extra filters applied were:

– news relevance: RELEVANCE = 100 (maximum relevance)

– news novelty: ENS = 100 (maximum novelty)

Testing the Thesis

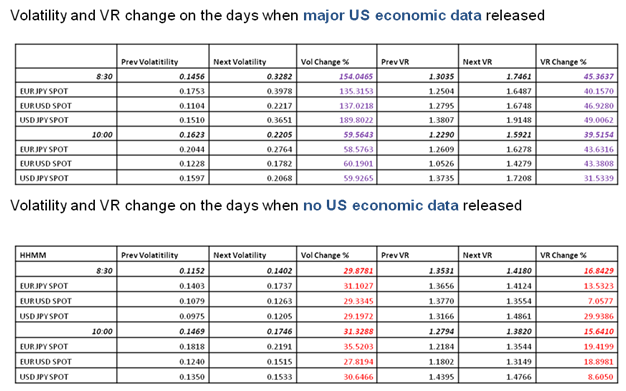

As a measure of volatility, we calculated the annualized standard deviation of log returns inside 5 minute windows of 10-sec bars (i.e. 30 bars). We also calculated variance ratio[i]:

VR = HILO (N) / ( ATR(N) * SQRT(N))

where

N = 30; HILO (N) is high/low price range and ATR(N) is average true range over the N bars period

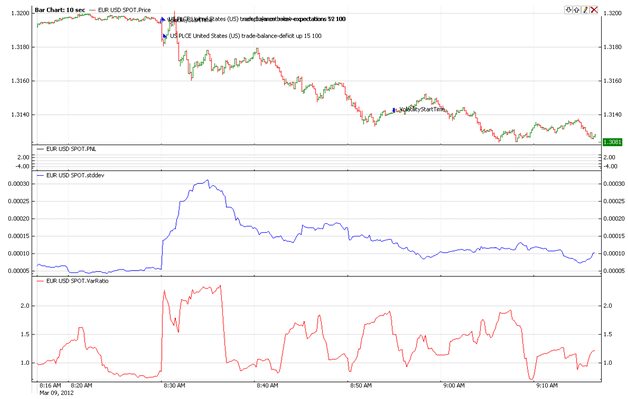

All statistics were calculated for 5 minutes before the time of the news release time and for 5 minutes after. For example, for US announcements scheduled for 8:30am, the time intervals were 8:25am to 8:30am and 8:30am to 8:35am. The results, pertaining to US economic news data, are show below:

Trading Strategy

It is clear from the results above that there is a significant change in short-term volatility of FX rates after the announcement of economic data. The next step in our research was to design and test a trading strategy which utilizes this observation.

The strategy defines breakout buy/sell levels in the five minute interval preceding the scheduled event. Upon receiving the news event, the strategy creates a long position if the price exceeds the buy level, and creates a short position if the market moves below the sell level. The strategy then closes positions five minutes after receiving the news event.

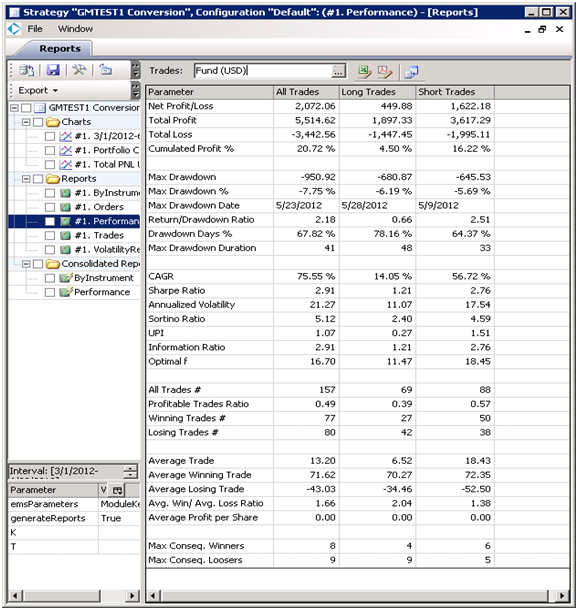

In back-testing, order execution simulation was done using the relatively conservative Best Bid Offer mode: buy at best ask price; sell at best bid price. The lot size for all trades was $100,000.

Results

[i] Variance Ratio statistics introduced by Lo and MacKinlay (1988):

VR close to 1 indicates that market is in a random walk regime;

VR > 1 indicates that market is in a trending regime (with positive autocorrelation of price returns);

VR < 1 indicates that market is in a mean reversion regime (with negative autocorrelation of price returns).

The Deltix Quantitative Research Team

Latest posts by The Deltix Quantitative Research Team (see all)

- Improving Order Execution in FX – Rethinking TCA - January 26, 2018

- Using Deltix for Trading Cryptocurrencies and Bitcoin Futures - December 11, 2017

- Advantages Of Recording Your Own Market Data - July 8, 2016