Examining Execution Transaction Costs in LME Metals

Transaction Cost Analysis (TCA) has traditionally been used to examine costs of order executions between different brokers, demonstrate best execution and provide other compliance-based functions. More recent applications of TCA involve forensic analysis of executions. This deeper analysis helps firms improve execution quality in the context of a specific trading strategy. To reflect the deeper analysis and internal focus, we call such studies Advanced Execution Analysis (AXA).

Research Methodology

Over the summer, we embarked on a study with our client, the London-based broker, Marex Spectron. The purpose of the study was to examine different methods of executing orders of six metals on the London Metal Exchange (LME) using an Advanced Execution Analysis approach.

Using Arrival Price (mid-price between bid & offer) as the benchmark, the study looked at whether increasing passivity can reduce transaction costs versus a market order. In addition to market orders, we tested variations in passivity via four different types of limit orders:

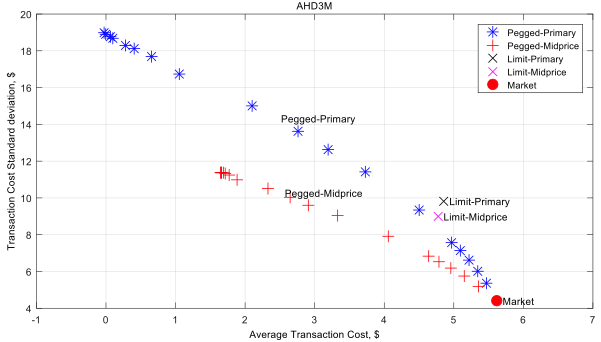

- Limit-Primary Places a limit order at the primary price level (bid for buy orders, offer for sell orders). If this order is not filled after 10 seconds, replaces the limit order with a market order. We use FIFO methodology for the order queue.

- Limit-MidPrice Places a limit order at the mid-price of the bid and offer, rounding down for buys and up for sells. We assume that our order is the first at that price level. Again, if the order is not filled after 10 seconds, we replace the limit order with a market order.

- Pegged-Primary Places a limit order at the primary price level and replaces on bid/offer updates. If the order is not filled over various time scales (from 1 second to 1 hour), it is replaced by a market order.

- Pegged-MidPrice Places a limit order at the mid-price and replaces on bid/offer updates. Again, if the order is not filled over various time scales (from 1 second to 1 hour), it is replaced by a market order.

Marex Spectron provided LME tick data for the six metals for the period March 1 to May 13 2016. This data together with corresponding market depth (order book) data and volume profile data was loaded into Deltix TimeBase. The different execution methods described above were implemented in Deltix QuantOffice and back-tested against the market depth data. The following statistics were computed:

- Transaction Cost (i.e. The difference between the order execution price and Arrival Price).

- Standard Deviation of Transaction Costs

- Average Time to Fill

- Limit Order Fill %

Results

Defining risk as the standard deviation of transaction costs, we found that:

- Across all evaluated strategies, the Market execution method has the highest expected transaction cost and the lowest risk associated with it.

- When using peg intervals of short duration (up to 30-60 seconds depending on the market), the Pegged-MidPrice execution method provides both lower expected transaction costs and risk compared to the Pegged-Primary execution method.

- Only Pegged-Primary (and not Pegged-MidPrice) demonstrates steady improvement of the transaction cost when using peg intervals of longer duration (above 60 seconds). However, this improvement comes at the cost of additional risk.

An example of results displayed graphically is shown below:

(Source: Marex, Deltix, LME)

The full study is available here.

Practical Considerations

As with any research, the results of one study are useful in providing general direction. However, the results would be significantly more useful if the research is repeated on an ongoing basis. This allows researchers to use market and trade data from different time periods, which will hopefully validate (or possibly repudiate) their results. At a minimum, ongoing research would help to refine their strategies.

For example, we are continuing this research by introducing price prediction heuristics into the pegged order execution methods. The goal is to reduce the risk of the Pegged-Primary method so we can capture the benefit of reduced transaction cost with less downside risk (i.e. standard deviation of transaction cost).

However, any price prediction technique is subject to the danger of curve-fitting. The on-going research approach described above extends the number and scope of out-of-sample testing periods to provide more reliable results.

Ideally, executions are analyzed in real-time. This way, researchers can analyze deviation of transaction costs versus benchmarks in the context of a rolling historical window (say from three months ago to real-time). With such information, traders can immediately identify divergences and execution anomalies compared to the performance of recent executions. This allows them to make necessary adjustments to ongoing executions or pending orders.

As we have discussed before, the holy grail is having fully adaptive execution algos which change their behaviour in real-time in response to real-time market data and actual performance. But the first step is to move from traditional TCA to ongoing detailed research and analysis of executions, so we can incorporate those findings into current trading decisions.

You can download this research study here.

More Insight on How To Do Execution Analysis

This research study is focused on advanced execution analysis rather than alpha generation. We’ll be publishing results of more execution research in 2017, so stay tuned.

In addition, over the summer, we published a couple of articles about approaches for doing advanced execution analysis. Here is a brief blog post discussing the advantages of recording your own market data for execution analysis. Here’s an article from Stuart Farr on DIY Execution Analysis published by CTA Intelligence.

If our research on signal generation is more relevant, you might find these research studies useful:

If you’d like to learn more about the platform used to conduct this research, visit our website or contact us.