Theoretical Background

The method of Index Tracking in portfolio management is a reproduction of time-dependence of a certain index I by distributing the capital among a given set of instruments S of the size M. To minimize transaction costs, the size N of a set P of instruments involved should not exceed certain boundary K. In this case the problem is called Tracking Portfolio Optimization with Cardinality Constraint. Here we describe how to apply Genetic Optimization (specifically, using the Genetic Optimization QuantOffice library) to solve the problem of Tracking Portfolio Optimization with Cardinality Constraint.

We use the following approach: the set P of allowed instruments and their weights  in the portfolio are found in course of genetic optimization. The fitness of the potential optimal portfolio is found as

in the portfolio are found in course of genetic optimization. The fitness of the potential optimal portfolio is found as

where  – weights of instruments representing the target index in the set S. If the target index corresponds to the instrument number k, then

– weights of instruments representing the target index in the set S. If the target index corresponds to the instrument number k, then  . For the covariance matrix C of individual instrument returns

. For the covariance matrix C of individual instrument returns

here  is the market price of the instrument m at time t.

is the market price of the instrument m at time t.

The genetic algorithm is as follows:

- Each possible solution to the Index Tracking problem is represented as a chromosome. The chromosome is a set P of instruments of size K and their weights . A population of such randomly generated chromosomes (randomly chosen instruments and weights) is maintained.

- Genetic optimization is performed in a number of iterations called generations. At the beginning of a new generation we have some initial population. All the chromosomes are sorted by their fitness to be a solution of the Index Tracking problem. The quantitative measure of fitness is the value of functional (1.1) for the weights of P.

- Having completed sorting, the best Elitism% chromosomes of population are selected for reproduction phase.

- Then the reproduction phase begins. Two chromosomes are selected at random and the crossover operator is performed on them yielding two children. This crossover procedure is repeated until there are enough children to replace the entire population except the best Domination% and the worst Mutation% chromosomes.

- The latter are subjected to the mutation operator.

- After a specified number of iterations the best chromosome P with weights of the last generation is reported as the Optimal Index Tracking Portfolio.

Genetic Operators

Crossover

Given two parent chromosomes A and B, the crossover operator generates two children  and

and  , according to the following procedure. Intersection

, according to the following procedure. Intersection  and symmetric difference

and symmetric difference  of the sets are calculated. Instruments which present in both portfolios A and B are assigned a weight SharedAllelesWeight. We start from empty children sets and . Then a random real number

of the sets are calculated. Instruments which present in both portfolios A and B are assigned a weight SharedAllelesWeight. We start from empty children sets and . Then a random real number  is played. If

is played. If

an element from I is chosen at random and added to the both children and . If

an element x from D is chosen at random. A second random real number  is played. If this number is less than 0.5 then x is assigned to . In the opposite case it is assigned to . The procedure with random number is repeated again and again until the both of the children reach the maximum size K. If any of the children and reaches the maximum size then all the subsequent assignments for that child are ignored.

is played. If this number is less than 0.5 then x is assigned to . In the opposite case it is assigned to . The procedure with random number is repeated again and again until the both of the children reach the maximum size K. If any of the children and reaches the maximum size then all the subsequent assignments for that child are ignored.

Mutation

The Mutation operator consists of a series of elementary mutations. The elementary mutations applied are of two types. Mutations of the first type are a sequence of random exchanges of the pairs of elements between the chromosome P and the complement S\P. During the second type of mutations a weight of randomly chosen instrument i is altered. The relative frequency of these mutations is regulated by InstrumentVsWeight parameter. Then intensity of mutation, i.e. how many instrument/weight pairs are modified during one mutation operator, is defined by NumberOfMutations parameter.

Strategy Usage Manual

As input, the strategy accepts a list of instrument symbols from which to choose the optimal portfolio, and the symbol of the target index (instrument). Which symbol corresponds to the target index is indicated in the “Target Instrument” field. Maximum size of tracking portfolio is indicated in “Maximum Size of Tracking Portfolio” field. The weights of instruments in the tracking portfolio can be constrained to have a unit sum,

as indicated by “Is weights sum constrained to be unity?” field. Sometimes it is desirable to remove this restriction since the value of target index is proportional to the value of portfolio, where the coefficient of proportionality is a slowly varying function of time.

The returns  of each instrument are calculated regularly over a fixed period of time, whose duration is specified in “Size of one History Time Step (days)” in days. All other duration parameters are specified in terms of this time step size.

of each instrument are calculated regularly over a fixed period of time, whose duration is specified in “Size of one History Time Step (days)” in days. All other duration parameters are specified in terms of this time step size.

The strategy accumulates the history of prices during “Length of Price History Window (Time Steps)” time steps. Then periodically at intervals of “Interval Between Portfolio Rebalance Events (Time Steps)” time steps the correlation function (1.3) is evaluated and GA is started. After GA is finished the optimal tracking portfolio weights are determined.

When the strategy is run it plots two price differences between the target index (instrument) and the tracking portfolio. The first price difference is reset after each rebalancing. The second price difference is reset only after the first rebalancing and shows how index (instrument) behavior is approximated by the tracking portfolio globally.

Genetic algorithm parameters are defined by the fields “Population size”, “Number of generations”, “Percent of Dominating Chromosomes”, “Percent of Elite” and “Percent of Mutated”. Their meaning is described above in the section ‘Method’.

Parameters of the index tracking genetic operators (see section Genetic Operators above) are defined by the following fields: “Shared Alleles Weight” is SharedAllelesWeight; “Number of Genes to Mutate at once” is NumberOfMutations; “Instrument vs Weight Mutations” is InstrumentVsWeight.

The size of a tracking portfolio is proportional to the transaction costs necessary to maintain it. So we should keep the portfolio as small as possible and discard negligible instruments. The field “Threshold Weight below which to discard Instrument” defines when the instrument is discarded from portfolio: the instrument j is discarded if the following is true:

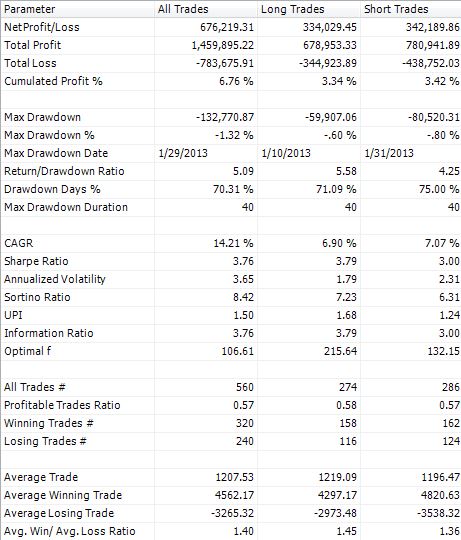

Example: “DIA” is specified as the index ticker. As a ticker universe, all the available equities are chosen. Maximum portfolio size e.g. = 4. All the other parameters are set as default in the current configuration of the attached strategy. The tracker approximates the out-of-sample behaviour of DIA; the quality of approximation is dependent on market (of course) and quality of data (gaps etc.).